If not yet enabled, enable and access the Roth Projection Tool.

Jump to:

Welcome to the Roth Projection

- Screen 1 of 3: Roth Conversion(s)

- Screen 2 of 3: Financial Asset Growth

- Screen 3 of 3: Spending and Inflation Assumptions

- Toggles/Warnings

- Report Headings/Clients/Assets

- Roth Conversion(s)/QCDs/General Assumptions/Medical Assumptions

- Client Assumptions

- Advisor Notes

Welcome to the Roth Projection

Upon entering a new Roth Projection, you'll be prompted to "Start" the three-step data entry wizard as seen below.

Screen 1 of 3: Roth Conversion(s)

Technically, the first input on screen 1 is for the Roth conversion amount, per taxpayer. While you certainly can enter that information on this screen, you aren't required to. Many advisors will wait until the wizard is complete to enter Roth conversion amounts based on the other data entered to better visualize Roth conversion opportunities.

In the example shown here, we demonstrate entering the conversion amounts later in the process in the Control Panel section, but the steps are identical.

In the first of three steps, you'll enter the information listed below:

- Taxable Assets - Enter the combined balance of all non-retirement accounts, including both cash and investments.

- Cost Basis of All Taxable Assets - Enter the cost basis of the taxable asset balance. This information is used to determine the tax impact of any taxable account distributions.

- Tax Deferred Assets - Enter the total balance for any tax-deferred assets that are subject to RMDs (Required Minimum Distributions) for Client 1 and Client 2.

- Combined Household Roth Assets - Enter the combined balance for any Roth accounts for Client 1 and Client 2.

-png.png?width=670&height=263&name=JoyOfRothing-Screen1-Roth%20Conversion(s)-png.png)

Screen 2 of 3: Financial Asset Growth

Next, assumptions will be made on the portfolio rate of return, tax efficiency of the portfolio, life expectancy, Social Security benefits start year, and the amount of each client.

- Rate of Return - Return assumption for the portfolio as a whole. Return by account type or for specific accounts is unsupported. We default to 8% arbitrarily

- Portion of returns that are capital gains (optional) - This assumption allows you to indicate how much of the rate of return is due to growth (which would not be taxed, to the extent that assets aren't sold to meet spending) and how much is due to income (which would be taxed at the end of the year, essentially defining the tax efficiency of the investments within the taxable assets account. A higher portion of returns that are assigned to growth ("capital gains") means less tax drag, making the taxable account more more tax-efficient. Keep in mind that the taxable assets balance may include not only investment positions but cash positions as well. The default value for this field is 20%, but that value is arbitrary and not reflective of Holistiplan's opinion on what should be entered here.

- Life Expectancy - Enter the life expectancy of each client. We arbitrarily default to age 100.

- Social Security Start Year - Enter the year when the client will begin receiving Social Security benefits

- Social Security Expected Amount - Enter the annual amount, in today's dollars, of the expected benefit amount once the client(s) begin receiving Social Security retirement benefits.

Screen 3 of 3: Spending and Inflation Assumptions

Screen 3 includes assumptions about annual spending, inflation, and whether adjustments are made for the embedded tax liability of tax-deferred accounts.

- Spending Assumption - Enter the annual spending assumption for your client's true lifestyle spending need for the first year of the projection. While the client may not need to spend any portfolio assets in the first year, entering a number is necessary to properly inflate spending throughout the projection when spending will potentially come from portfolio sources.

The Spending Assumption is entered annually and will be satisfied by income in the following order:

- Income (Wages, Social Security, Pension, or Annuity), entered later

- Portfolio Distributions (taxable first, then tax-deferred, then Roth)

NOTE: Once your client reaches RMD (Required Minimum Distribution) age, then RMDs are the first component of portfolio distributions that are used, not taxable accounts.

- Inflation Assumption - Enter the assumed inflation assumption for tax brackets and the standard deduction amount. Inflation assumptions for spending and income items are added for each of those items individually, and not in this field.

- Tax Adjustment Assumption for Tax-Deferred Accounts (optional) - This setting effectively reduces the tax-deferred balances by the amount of the percentage indicated to reflect the embedded tax liability for those accounts. For example, if the total balance for all tax-deferred accounts were $1,000,000, and the tax adjustment assumption was set to 24%, the adjustment to the tax-deferred account balances would reduce them by 24% ($240,000), and effectively use a new balance of $760,000 in the projections to account for the after-tax funds available from those accounts. This setting can be toggled on/off now or at any time in the future within the projection within the Control Panel.

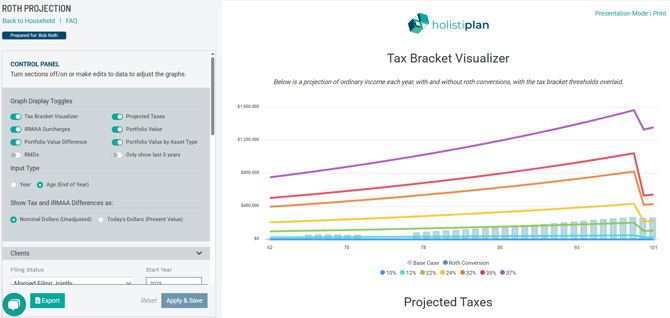

The Control Panel

Once the Roth Projection wizard is completed, your Roth Projection will look like the example below.

The Control Panel will be on the left side of your screen, where you can make edits to assumptions and other changes. The right side of your screen will show a preview of the Roth Projection output, complete with your firm logo and any disclaimer language.

You will also see buttons at the top right of the preview panel to view the Roth Projection in Presentation Mode (without the Control Panel) and to print the Roth Projection.

Before diving into the results, first review the Control Panel for additional settings and assumptions.

Toggles / Warnings

- Toggles: Toggles exist to show or hide the Tax Bracket Visualizer, Projected Taxes, IRMAA Surcharges, Portfolio Value, Portfolio Value Difference, Portfolio Value by Asset Type, and RMDs section, as well as only to show the last 5 years of portfolio balance estimates. You can also choose to input data by the calendar year or client age, and to show tax and IRMAA differences in nominal dollars (unadjusted) or today's dollars (net present value using the inflation assumption as a discount rate), depending on what makes the most sense for you.

- Warnings: These cautionary warnings indicate when some entries were not modeled fully as intended, due to calculations made within the analysis. Any warnings preventing the Roth Projection analysis from being completed will appear in red at the top of the Roth Projection page.

Report Headings / Clients / Assets

- Report Headings: Adjust the name of your Roth Projection by changing the title here, along with any subtitle you wish to apply for client presentation purposes.

- Clients: Adjust the filing status, clients representing Taxpayer 1 and Taxpayer 2, the year, and show if either taxpayer is eligible for the additional standard deduction for blindness.

- Assets: Make any edits to the balance for taxable assets, cost basis of those taxable assets, tax-deferred asset balance(s), and combined Roth assets balance(s).

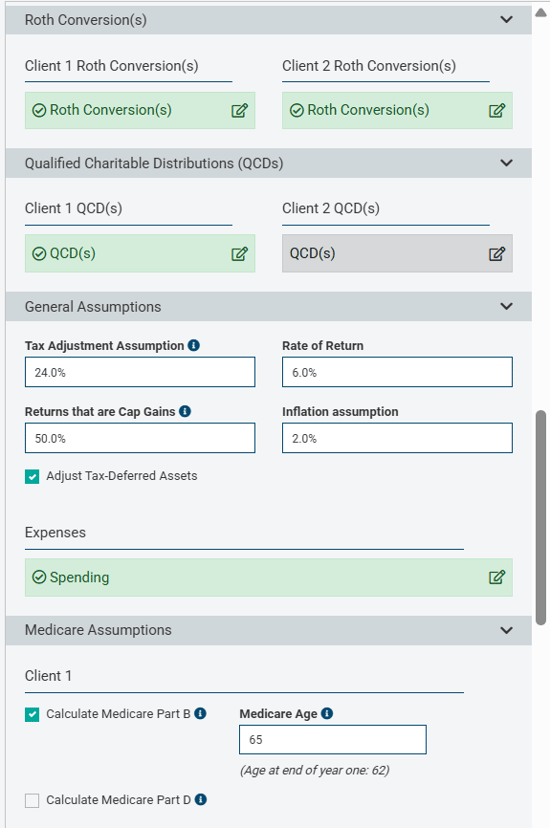

Roth Conversion(s) / QCDs / General Assumptions / Medical Assumptions

- Roth Conversion(s): Adjust the amount and sequencing of the planned Roth conversions for your client(s) here.

Click the pencil/paper icon to open the Roth Conversion screen. Similar to other screens in this tool, click +Add Row to add the first row for the year you wish to begin conversions, along with the amount and any corresponding inflation adjustment for future years. Be sure to indicate when you use conversions to end, otherwise the system will assume that conversions continue indefinitely. In the example below, the client is performing a $50,000 conversion in the first year of the projection, inflated at 3% per year, for 10 years.

- Qualified Charitable Distributions (QCDs): Enter any amount of QCDs your client is using as a charitable giving strategy.

In the example below, we have added $20,000 of QCDs for Client 1 beginning at their age 71 and continuing indefinitely. We have inflated these QCDs at 6% (the same as the return rate) in order for the QCD amount to increase at the same rate the account is projected to grow over time.

NOTE: For cash flows you want to end, you will want to add a row and enter the year you wish for the cash flow to end, along with a "$0" in amount column. Otherwise, the system will think that the cash continues indefinitely. In the example above, the system assumes this to mean that QCDs will continue in an inflation-adjusted manner until the client dies.

Holistiplan will alert you and generate an error if you attempt to enter QCDs for a client who will not be 70.5 at the end of that tax year, since QCDs are not allowed until the taxpayer has attained the age of 70.5. That warning will look like the one below.

- General Assumptions:

- Tax Adjustment Assumption: This setting effectively reduces the tax-deferred balances by the amount of the indicated percentage to reflect the embedded tax liability for those accounts. For example, if the total balance for all tax-deferred accounts were $1,000,000, and the tax adjustment assumption was set to 24%, the adjustment to the tax-deferred account balances would reduce them by 24% ($240,000), and effectively use a new balance of $760,000 in the projections to account for the after-tax funds available from those accounts.

- Rate of Return: This assumed return is applied to all account types as a blended rate within the investment portfolio - taxable, tax-deferred, and Roth.

- Returns that are Cap Gains: This assumption approximates the growth/income nature of investments within the taxable assets account. The higher the portion of returns reflect "capital gains" (e.g., growth), the less tax drag the taxable account will experience, making it more tax efficient. Keep in mind that the taxable assets balance may include not only investment positions but cash positions as well.

- Inflation Assumption: This setting adjusts the inflation assumption for tax brackets and the standard deduction amount. Inflation assumptions for spending and income items are added for each of those items individually, and not in this field.

- Adjust Tax-Deferred Assets Checkbox: Checking this box incorporates the Tax Adjustment Assumption above to reduce the starting balance of the total tax-deferred assets by the percentage entered in that field.

-

- Expenses: Use this field to edit the spending assumption for your client's true lifestyle spending need for the first year of the projection. While the client may not need to spend any portfolio assets in the first year, entering a number is necessary to properly inflate spending throughout the projection, when spending will potentially come from portfolio sources. Be sure to add a new row/year for when expenses may change - up or down - outside of any inflation adjustment from the previous year. An example may be a large purchase in a given year (which would cause spending to increase beyond an inflation adjustment), or if expenses decreased due to downsizing, the death of a member of the household, or some other reason.

- Medicare Assumptions (optional):

- To include the impact of any Income Related Monthly Adjustment Amount (IRMAA) surcharges, check the box for Medicare Part B and/or Medicare Part D for Client 1 and Client 2 (if filing jointly).

- Enter the age Client 1 is planning on enrolling in Medicare (usually age 65, though this may not be the case if they are still working and covered by their employer's plan and not required to enroll in Medicare until retirement).

- Enter the Medicare Part D Annual Premium. Unlike Part B, Part D Medicare Premiums vary by plan choice and zip code, so there is no uniform amount.

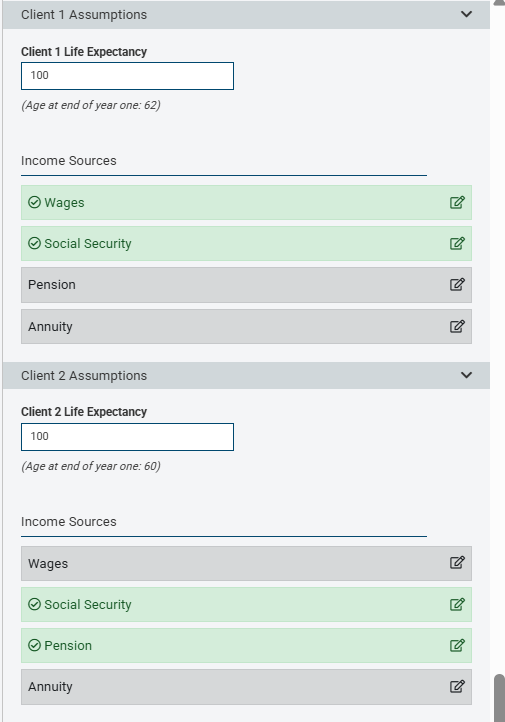

Client Assumptions

- Life Expectancy: Use this field to update the life expectancy of your client(s). The projection's end date corresponds to the user-entered life expectancy for the longest-lived member of the household.

- Income Sources: Income sources are the first source used to meet spending needs, so confirm that any income from the sources below is entered.

- Wages

- Social Security

- Pensions

- Annuities

Taxable Accounts > Tax-Deferred Accounts > Roth Accounts

NOTE: Once your client reaches the age when Required Minimum Distributions (RMDs) begin, those RMDs will comprise the first component of portfolio distributions, followed by taxable accounts.

In the example below, we have added $150,000 of Wage Income for Client 1 for two years, beginning at age 62, increasing by 2.0% per year, and ending at age 64.

NOTE: For cash flows you want to end, you will want to enter a "$0" amount in the year following the last year of that series of income. Not entering a "$0" amount will cause that cash flow stream to continue indefinitely.

Notice that there is a graph below the entry rows showing you the shape of that income, and by hovering over the graph, you can verify the income is occurring in the years and in the amounts you intended.

Advisor Notes

Use this section as a spot to jot any notes for yourself about your analysis. The "Advisor Notes" section is not shown in the report, so these notes will not print when creating a PDF deliverable for your client, or when viewing the Roth Projection analysis in Presentation Mode.

We have a separate article to help explain the various outputs of the analysis here: Interpreting the Results