In general, Form W-2 records compensation paid by an employer to an employee, from which a combination of income taxes, Social Security taxes, and Medicare taxes may be withheld.

Jump to:

Anatomy of a W-2

Example W-2

Taxation by Compensation Type

Review a blank Form W-2, which includes a detailed explanation of each box and codes that may be seen on a W-2, and the Instructions directly from the IRS. We've included an overview of the more commonly used boxes below.

Anatomy of a W-2

- Box 1 (Wages, tips, other compensation): This is where taxable wage income is reported, and the number seen flowing through to line 1a of Form 1040. This amount reflects all pre-tax payroll deductions, such as pre-tax 401(k) contributions, payroll contributions to Health Savings Accounts (HSAs), Flexible Spending Accounts (FSAs), etc.

- Box 2 (Federal income tax withheld): Federal income tax withholdings listed here can be entered in the field for Federal Withholding, which will populate within the Withholding Calculator at the bottom of the screen in Scenario Analysis.

- Box 3 (Social Security wages): Certain compensation may be exempt from income taxation (e.g., pre-tax 401(k) salary deferrals), but is still subject to payroll taxes, or FICA (Federal Insurance Contributions Act) withholding. Additionally, there is a Social Security Wage base ($184,500 for 2026), after which no additional compensation is taxed fr purposes of the Social Security portion of FICA.

- Box 4 (Social Security tax withheld): This should equal Social Security wages (up to the Social Security Wage Base mentioned in the previous bullet point) multiplied by the Social Security tax of 6.20%. Because this does not show up on the tax return, with some exceptions detailed in this article, entering FICA withholding in Holistiplan is not necessary. Sometimes, when there are multiple employers with two payroll services involved, clients may have over-withholding of Social Security taxes. In that case, that amount over-withheld is captured as a non-refundable credit on Line 11 of Schedule 3.

- Box 5 (Medicare wages and tips): Unlike with Social Security taxes, Medicare taxes are due on most income (with no cap like Social Security wages), including items not subject to income taxes (e.g., pre-tax 401(k) salary deferrals). Section 125 Cafeteria Plan contributions, like payroll contributions to HSAs and FSAs, along with disqualified dispositions of Incentive Stock Options (ISOs), are excluded from both Social Security taxes and Medicare taxes.

- Box 6 (Medicare tax withheld): Medicare tax is withheld at 1.45% up to a threshold depending on filing status ($200,000 for single, head of household, or qualifying spouse; $250,000 for married filing jointly, and $125,000 for married filing separately). An Additional Medicare tax rate of 0.9% applies to those wages over the applicable threshold. Additional Medicare Tax is calculated on Form 8959.

- Box 12: Boxes 12a through 12d may list several items. A legend for what these codes mean is found on the reverse of the full version of the W-2.

- Box 13: These check boxes will indicate whether the taxpayer is considered a statutory employee, is covered by an employer-sponsored retirement plan, and/or received sick pay from a third party. If the Retirement Plan box is checked, deductions for contributions to a Traditional IRA may be limited. For more details, check out IRS Publication 590-A.

- Box 14 (Other): Employers use this box for several items and to note special situations.

- Box 15, 16, and 17: These boxes will list the state (Box 15), state tax ID of the employer, state wages if different than Box 1 (Box 16), and state income taxes withheld (Box 17). Learn about state taxes in Holistiplan here.

- Box 18, 19, and 20: Some taxpayers live in municipalities that levy a local income tax. These boxes will identify any local wages if different than Box 1 (Box 18), any local income taxes withheld (Box 19), and the name of the municipality (Box 20).

Often, an example is helpful, so let's look at one below. Huey Lewis is working for a living. His employer pays him a gross salary of $350,000 and provides him with the following W-2 for 2026.

- Box 1: Huey's wages of $316,870 reflect his gross salary of $350,000, less:

- $20,000 in pre-tax 401(k) contributions (Line 12b),

- $4,850 in HSA contributions made via payroll (Line 12d), and

- $8,280 in employee-paid health insurance premiums. Keep in mind the amount listed on Line 12c with a code of "DD" reflects the total cost of employer-provided health insurance coverage, not just the tax-exempt employee-paid premiums. To find out the mix of employee vs. employer costs, best bet is to review a paystub.

- Box 2: Huey withheld a flat 35% of his taxable earnings for a total of $120,803.

- Box 3: Although Huey's wages were well in excess of $184,500, that's the Social Security wage base for 2026, so his Social Security wages are capped at that amount.

- Box 4: Likewise, the employee side of the Social Security taxes (6.20%) that are withheld stop once he reaches the wage base.

- Box 5: Huey's Medicare wages equal his gross salary ($350,000) less his only FICA-exempt item, the $4,850 contributed to his HSA via payroll as reported on Line 12d.

- Box 6: Since Huey's a single filer and his Medicare wages in Box 5 are over the threshold for single filers ($200,000), Huey will owe 1.45% on the first $200,000 in wages ($2,900) and 0.9% on the remaining $145,150 of wages ($1,306) to arrive at a total Medicare tax withholding of $4,206.

- Box 12 Items:

- 12a (Code: AA): Huey made $10,000 of Roth 401(k) contributions before his advisor recommended switching to pre-tax 401(k) contributions to lower his tax bill. Those $10,000 Roth contributions are reflected here and included in the wage figure in Box 1 and the Medicare Wages figure in Box 5.

- 12b (Code: D): Huey switched to pre-tax contributions to his 401(k) during the year and ended up making $20,000 (12,500 of his deferral limit + the $7,500 catch-up contributions due to his ripe old age of 72 at the time of this writing) of pre-tax 401(k) contributions. These salary deferrals reduced his wages in Box 1, but not his Medicare wages in Box 5, since elective retirement plan deferrals are subject to FICA.

- 12c (Code DD): Huey's employer provides a health insurance plan. However, the $33,120 listed here reflects the full (employer and employee) cost of this health insurance coverage. The employee portion, determined by reviewing Huey's paystub, was $8,280 (or 25%). That portion paid by Huey was excluded from his wages in Box 1. Since employer-provided health insurance benefits are classified as a Cafeteria Plan benefit under Section 125 of the federal tax code, that amount is also exempt from FICA taxes as well, and is not included in Social Security wages (Box 3) or Medicare wages (Box 5).

- 12d (Code W): Huey's employer also contributes a portion of his wages to an HSA. Those contributions reduce his wages in Box 1, and are not subject to FICA taxes, and are not included in Social Security wages (Box 3) or Medicare wages (Box 5).

While HSA contributions made via payroll deductions are not subject to FICA taxes, HSA contributions made out-of-pocket are not exempt from FICA taxes, since after-tax money is used to contribute. The corresponding income tax deduction is claimed on Line 13 of Schedule 1 when filing a return.

- Box 13: Huey has the box checked for "Retirement plan" due to him being covered by his employer-sponsored 401(k) plan. His ability to deduct Traditional IRA contributions is limited as a result, and because his income is so high, he cannot deduct any contributions made to his Traditional IRA.

- Box 15, 16, and 17: Huey's state wages are the same as his wages subject to federal income taxes (and equal to Box 1). However, if the state taxes more or less of that Box 1 income, Box 16 can be different. Huey had a flat 10% of his wages withheld for California income taxes for a total of $30,687.

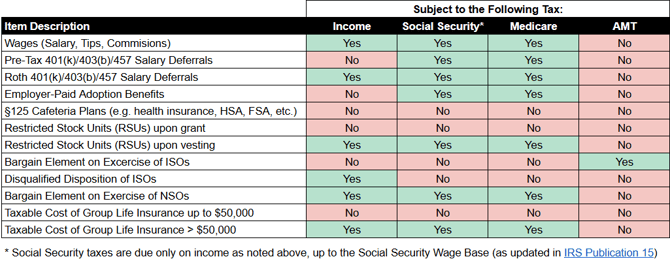

The chart below may be a useful reference point to help remember what portions of wage income are subject to which tax.