By default, Holistiplan displays a combined total in the Wages from 1040 Line 1 field based on the uploaded return.

-

To enable per-taxpayer entry: The Wages from 1040 Line 1 field must be completely cleared. This means the field must be completely blank; entering "0" will keep the individual taxpayer rows hidden.

Projecting Income (The Income Annualizer)

When a scenario requires projecting full-year income based on a mid-year paystub, the Income Annualizer tool can provide the necessary calculations.

-

Access: Select the Income Annualizer link located at the top of each taxpayers' respective column of the Wages Worksheet.

-

Functionality: Inputting Year-to-Date (YTD) totals and the Pay Period End Date allows the system to extrapolate those figures into a full 12-month projection.

-

Application: Once the projection is calculated, the Apply to Worksheet button pushes the annualized Gross Wages, Pre-tax Deferrals, and Withholding directly into the respective Taxpayer 1 or Taxpayer 2 columns.

Learn more about the Income Annualizer and Pay Stub Scanner here: Income Annualizer and Pay Stub Scanner.

Mapping Compensation Types

The following table provides the correct placement for common W-2 and paystub line items to ensure accurate tax modeling.

| Compensation Type | Entry Field | Tax Impact |

| Salary / Hourly | Gross Wages | Subject to Income Tax & FICA |

| Qualified Overtime | Qualified Overtime Income | Subject to Income Tax & FICA; possible OBBBA deduction |

| Qualified Tips | Qualified Tip Income | Subject to Income Tax & FICA; possible OBBBA deduction |

| Annual Bonus | Bonus | Added to Gross; Subject to Income Tax & FICA |

| RSU vesting; Bargain element of Non-qualified | RSUs | Added to Gross; Subject to Income Tax & FICA |

| Bargain element of Non-qualified Stock Option Exercise | NQSOs | Added to Gross; Subject to Income Tax & FICA |

| Pre-tax 401k/403b/457/401a Plan Contributions | Pre-tax Retirement Deferrals (401k/403b/SIMPLE) | Reduces Income Tax; Still subject to FICA |

| HSA /FSA/Health, Medical, and Dental Premiums (Section 125 Plans) | Section 125 / Other Pre-tax Deds. Not Subject to FICA | Reduces Income Tax & FICA |

| Non-Qualified Deferred Compensation (NQDC) Distributions | Deferred Compensation Distributions | Subject to Income Tax; Exempt from FICA |

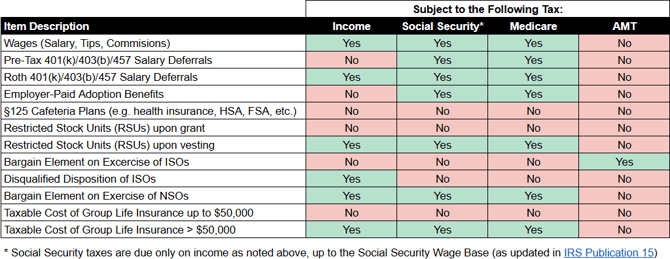

The chart below may be a useful reference as a reminder of which taxes are applicable to various forms of wage income.

FICA and Medicare Exemption Logic

For cases involving clergy, certain government employees, or specific visa holders, wages may be exempt from standard payroll taxes. The worksheet includes specific toggles for these scenarios.

-

Wages Exempt from Social Security Payroll Tax: Selecting this checkbox prevents the calculation of the 6.2% Social Security tax on the entered wages.

-

Wages Exempt from Medicare Payroll Tax: Selecting this checkbox prevents the calculation of the 1.45% Medicare tax.

Understanding Calculated Fields

Holistiplan uses the data entered to populate two fields, each of which is outlined in red in the accompanying screenshot. These fields are read-only and update in real-time.

Wages Used In Income Tax Calculations

This represents the final figure flowing to Form 1040, Line 1.

-

The Formula: [Gross Wages] + [Qualified Tips] + [Qualified Overtime] + [Bonus]— [Pre-tax Savings Deferrals] — [Other Pre-Tax Deductions Subject to FICA] - [Pre-tax Section 125 Deductions]+ [RSUs/NQSOs] + [Non-Qualified Deferred Compensation] .

Medicare Wages (Form 8959 Line 1)

This field determines if the taxpayer is subject to the 0.9% Additional Medicare Tax.

-

The Formula: [Gross Wages] — [Pre-tax Section 125 Deductions] + [Annual Bonus] + [RSUs/NQSOs] + [Qualified Tips] + [Non-Qualified Deferred Compensation].

-

Note: Unlike taxable wages, Pre-tax Savings Deferrals (e.g., 401k contributions) do not reduce Medicare wages

Modeling Additional Medicare Tax

Once wages are assigned to a specific taxpayer, the system automatically calculates payroll taxes:

-

Social Security: Calculated at 6.2% up to the annual wage base.

-

Medicare: Calculated at 1.45% on all Medicare wages.

Additional Medicare Tax (Form 8959): To ensure this 0.9% tax is calculated correctly for high earners, the Medicare Wages override field (Form 8959 Line 1) must be cleared. This allows the system to use the broken-out taxpayer data from the worksheet rather than the 1040 aggregate.

Once that override field is cleared and the box is blank, the Medicare Wages for each taxpayer populate, and the calculated Additional Medicare Tax will adjust accordingly.

Tax Withholding

Withholding entered in this worksheet flows directly to the Withholding section of the main Scenario Analysis screen.

-

Federal Withholding: Enter the annual projected amount for Federal income tax withheld.

-

State Withholding: Enter the annual projected amount for State income tax withheld. You must select and add the state scenario to be able to add state tax withheld.

-

Automation: If the Income Annualizer is used, these fields will be pre-populated with projected totals based on YTD figures.

Troubleshooting & FAQ

Why is the Taxable Wages field different from the gross entry? The Taxable Wages field subtracts Pre-tax Deferrals and adds items like Stock/Bonus income. It also accounts for Qualified Overtime exemptions.

Where are Schedule C or K-1 earnings entered? These are not W-2 wages. Utilize the Schedule C or Schedule E worksheet links located in the main Income section of Scenario Analysis.