A 529 plan is often used by parents, grandparents, etc. to help cover education expenses for a beneficiary, such as a child, grandchild, niece, nephew, or even for themselves. The money contributed to these plans grows and can be withdrawn tax-free, provided it is used for qualified higher education expenses (QHEE). These expenses can include tuition and fees, certain electronics, books and classroom equipment, and some room and board costs. You can find more details on QHEEs by visiting the IRS resource linked below.

Topic No. 313 Qualified Tuition Programs (QTPs)

However, there are times when 529 funds may be used for non-qualified expenses and/or when funds are used for an amount that exceeds the qualified higher education expenses amount. In those instances, the earnings on these distributions are subject to additional taxes as outlined by the IRS.

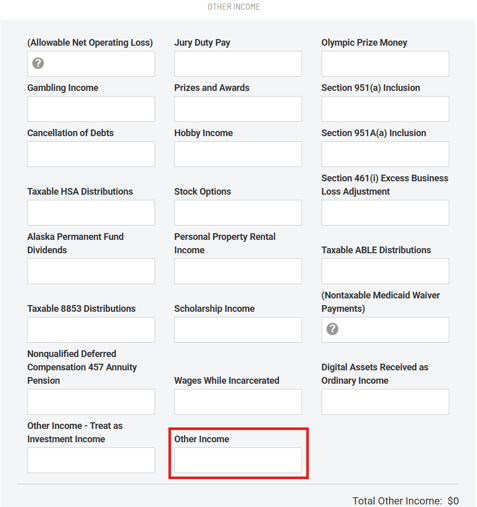

To model the taxable portion of the distribution from a 529 plan, navigate to the Other Income worksheet within the Schedule 1 Income section of Scenario Analysis. Enter the taxable amount of those distributions in the field circled below to reflect the tax implications.

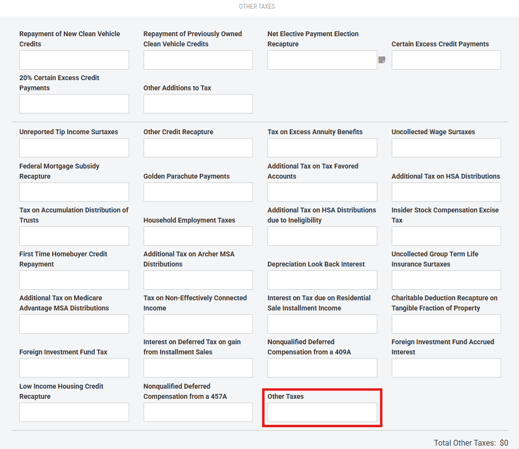

Additionally, if any or all of the distribution will be subject to the 10% penalty, enter that additional 10% penalty in the Other Taxes worksheet within the Other Taxes section of Scenario Analysis.

Holistiplan will not calculate that penalty amount. This will need to be done manually outside the software, and then entered where shown above.

As many states use Federal AGI or Federal Taxable Income as a starting point for the state tax calculation, any income included in the Other Income section from these 529 Plan distributions are already included in Federal AGI and Federal Taxable Income, and does not need to be added in the state taxes section of Scenario Analysis. Check the state taxing authority's website in question to confirm if any additional state tax implications of these non-qualified 529 Plan distributions apply.