Overview

Taxpayers who adopt a child may be eligible for a tax credit for adoption-related expenses up to a specific dollar amount. This article describes how users can determine the amount of the Adoption Credit in Scenario Analysis, including:

- Calculation of the credit per child, including income-related phase-outs

- Support for data entry for multiple children

- Inclusion of data fields for carryforward credit amounts from prior years

- Determination both non-refundable and refundable portions

- Computation of any carryforward amount for future years

This credit is calculated on IRS Form 8839. The credit is available to taxpayers of all filing status, with the exception of Married Filing Separately (unless certain circumstances apply).

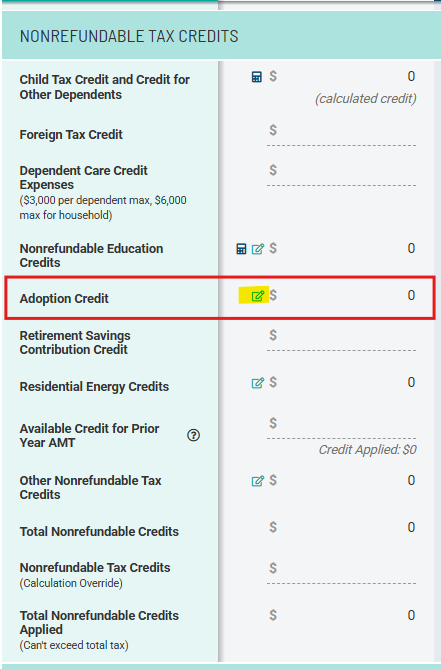

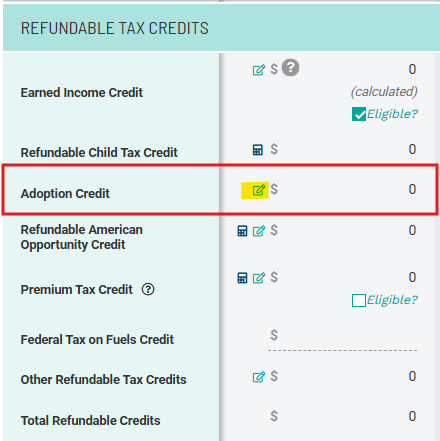

Users can access the Adoption Credit dialog box in either the Nonrefundable Tax Credits or Refundable Tax Credits section within Scenario Analysis.

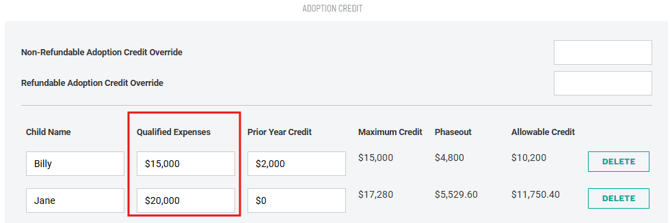

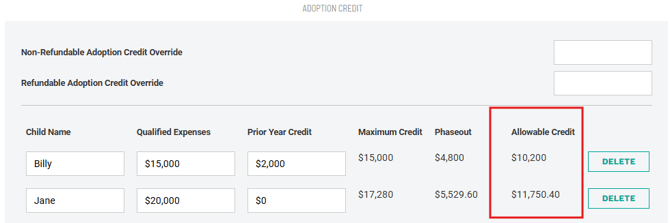

Qualified Expenses

Start by entering the qualified expenses for any adopted children. Qualified expenses include:

- Adoption fees

- Attorney fees

- Court costs

- Travel expenses (including meals and lodging) while away from home

- Other expenses directly related to, or for the principal purpose of, the legal adoption

- Expenses paid before identifying an eligible child, such as home study fees

The amount of qualified expenses to enter depends on the timing of the expenses and whether the adoption involves a foreign child or a special needs child. Special rules apply in these cases, see the Form 8839 Line 5 instructions for guidance on the correct amount.

The amount of any expenses reimbursed by an employer under a qualified adoption assistance program are not qualified adoption expenses and are therefore not eligible for the credit. Accordingly, back out any reimbursed expenses from the amount of qualified expenses entered.

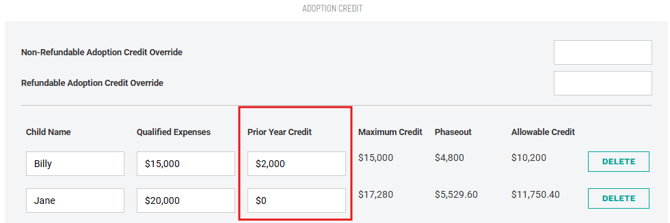

Prior Year Credit

The amount of the credit is technically per child, not per year. If the adoption and corresponding expenses span multiple years, adjust the amount of any calculated credit in the current year by credits claimed in prior years.

If a client filed Form 8839 for a prior year for the same child, enter the total of the amounts from lines 3 and 6 (or the corresponding lines) on the last Form 8839 filed for that child, essentially reflecting the amount of the credit the taxpayer has already claimed for the adoption of the child.

Allowable Credit per Child

Once the qualified expenses and any prior year credit amounts have been entered, Holistiplan calculates the maximum credit per child for the current year, along with any income-related phaseouts and the resulting allowable credit.

Any phaseout is determined by Modified Adjusted Gross Income (MAGI), defined broadly as AGI plus any amount of excluded income from Puerto Rico or determined by Foreign Earned Income Exclusion. The MAGI threshold adjusts annually for inflation and is the same amount for all filing statuses.

Unused Credits Carried Forward From Prior Years

The amount of any credit claimed in the current year can include unused amounts carried forward from the previous five years. Similarly, any unused portion of the nonrefundable credit for the current year can be carried forward to future years.

Holistiplan provides fields for any carryforward amounts from previous year at the bottom of the Adoption Credit modal. Users will need their clients’ Adoption Credit Carryforward Worksheet (found in the prior year’s Form 8839 instructions or ideally included with a client’s tax return) to determine these amounts, as Holistiplan does not read that worksheet when analyzing an uploaded return.

Without this information, users may end up calculating an incorrect amount for the adoption credit in the year of your scenario.

Nonrefundable and Refundable Credit for the Year

Starting in 2025, a portion of the credit will be considered refundable, with the rest considered nonrefundable. Holistiplan displays both amounts in the Adoption Credit worksheet, as well as in the respective sections for each type of credit in the main Scenario Analysis screen. We will also indicate the amount of any carryforward amount of nonrefundable credit for future years.