The One Big Beautiful Bill Act (OBBBA) that was signed into law on July 4, 2025, extends some provisions of the tax regime first introduced with the Tax Cuts and Jobs Act (TCJA), while also introducing new deductions and making some tweaks to TCJA-related items. This article summarizes the changes specific to what can be modeled in Scenario Analysis (and visualized in Range Calc), acknowledging that there may be other provisions of the bill that apply to estate taxes, corporate taxes, and other elements beyond the current scope of what folks can model in Holistiplan.

Caution: The information presented in this article (and in the software) is based on our best understanding of the provisions found in H.R. 1 (https://www.congress.gov/bill/119th-congress/house-bill/1/text). These interpretations may change over time with additional information and further guidance from the IRS.

Jump to

Calculation Options

Extension of Current Marginal Brackets on Ordinary Income

Extension of Higher Standard Deduction Amounts

State and Local Taxes (SALT) Deduction

Limitation on Itemized Charitable Deductions

Limitation on Total Itemized Deductions

Extension of higher individual AMT exemption levels established by the TCJA

Adjustments to Section 199A (Qualified Business Income Deduction)

New Deductions

Charitable Deductions for Taxpayers Not Itemizing

No Tax on Tips

No Tax on Overtime

Enhanced Senior Deduction

Auto Loan Interest Deduction

New or Enhanced Credits

Child Tax Credit

Adoption Credit

Scholarship Credit

Wrap-Up

Calculation Options

The Current Law calculation option will be the only option available for 2026 scenarios and beyond by default.

As of January 1, 2026, TCJA calculations are no longer supported. Users should receive a message like the one shown below when accessing Scenario Analysis, prompting them to save any projections using that TCJA calculation option.

Extension of Current Marginal Brackets on Ordinary Income

The 10%, 12%, 22%, 24%, 35%, and 37% brackets on ordinary income from the Tax Cuts and Jobs Act (TCJA) continue and are now permanent. The previously published brackets for 2025 remain and will be adjusted for inflation in 2026 and beyond. Moreover, the 10% and 12% brackets receive an additional bonus inflation adjustment in 2026, effectively giving them a two-year inflation adjustment.

Extension of Higher Standard Deduction Amounts

The OBBBA maintains and increases the higher standard deduction amounts from the Tax Cuts and Jobs Act (TCJA) and makes the higher amounts permanent. These standard deduction amounts will continue to be adjusted for inflation in future tax years.

Additionally, taxpayers who are age 65 and older and/or blind remain eligible for additional standard deductions, as applicable. They may also be eligible for a new enhanced senior deduction (discussed later) in addition to the base and additional standard deduction amounts.

2025 Standard Deduction Amounts:

- $15,750 - Single

- $23,625 - Head of Household

- $31,500 - Married Filing Jointly

- $15,750 - Married Filing Separate

- $31,500 - Qualifying Surviving Spouse

EXAMPLE: Robert and Roxanne are a couple using the Married Filing Jointly filing status. They are both age 70, and neither is blind. In 2025, they would be eligible for the following standard deduction:

$31,500 - Base Standard Deduction for Married Filing Jointly Filer

+ $1,600 - Additional Standard Deduction for Robert being 65 or older

+ $1,600 - Additional Standard Deduction for Roxanne being 65 or older

$34,700 - Total Standard Deduction

Any additional enhanced senior deduction (discussed later) would be in addition to the $34,700 standard deduction in the example above, and can be found in the Other Deductions and QBI section of Scenario Analysis.

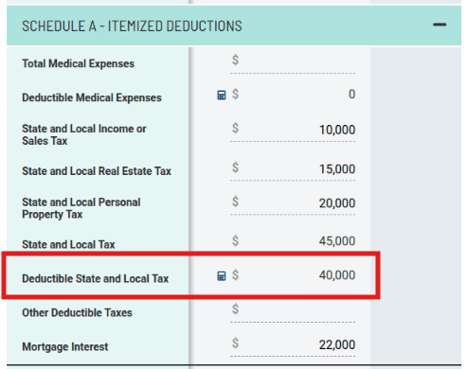

State and Local Taxes (SALT) Deduction

Under the TCJA, taxpayers were limited to a deduction of $10,000 for state and local taxes (SALT), regardless of income. Under the OBBBA, in 2025, taxpayers can now deduct up to $40,000 of SALT ($20,000 for married filing separately filers), subject to phase-out. These amounts are adjusted for inflation by 1% through 2029.

Higher-income taxpayers may see a limit on these deductions, as they begin to phase out by 30% when MAGI exceeds a particular income amount based on filing status:

- MFS: Starts at $250k, fully phased out at $300k

- Others: Starts at $500k, fully phased out at $600k

Note that in this context, “fully phased out” means that the taxpayer will still receive the minimum SALT deduction of $10,000 ($5,000 for MFS). These phase-out thresholds are also adjusted by 1% more than the preceding year and will be inflation-adjusted annually (starting in 2026 at 101% of the prior year).

In the example below, for a 2025 Married Filing Jointly scenario, the taxpayers have $45,000 of State and Local Tax; however, due to income limitations, they are entitled to a deduction of $26,125:

Clicking the calculator icon next to the deduction amount will show the calculation for the limitation in the deduction.

The maximum SALT deduction reverts to the $10,000 ($5,000 for MFS) under TCJA in 2030 and beyond, subject to additional legislative changes.

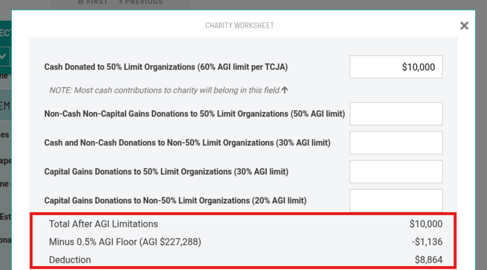

Limitation on Itemized Charitable Deductions

Starting in 2026, taxpayers will be subject to a floor of 0.5% of AGI for itemized charitable deductions. Holistiplan will automatically calculate the limited charitable deduction:

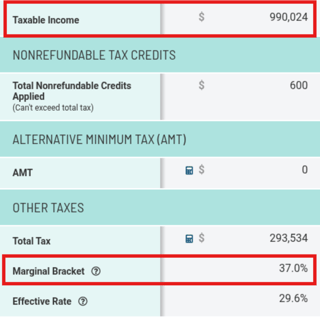

Limitation on Total Itemized Deductions

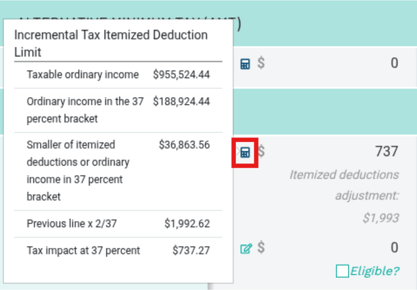

For tax years 2026 and beyond, taxpayers in the 37% bracket will experience a limitation on their itemized deductions. For these taxpayers, itemized deductions will be reduced by 2/37ths of the lesser of:

- The total itemized deductions, or

- The amount of taxable income that surpasses the threshold where the 37% marginal bracket on ordinary income begins (all taxable income taxed above the 35% bracket).

The bill text does not specify where this calculation is going to take place on a tax return. Because this limitation is based on taxable income rather than Adjusted Gross Income, it may not work like the old pre-TCJA Pease limitations, where the adjusted amount of itemized deductions was a specified line item on Schedule A.

Accordingly, to simplify our internal calculations, we have constructed a workaround. Users can continue to enter the gross amount of itemized deductions, and Holistiplan will show those gross deductions without adjustment. Further down the page, we will calculate the implied taxation on the limited deduction amount, resulting in the same total tax as if the deductions had been automatically limited on Schedule A.

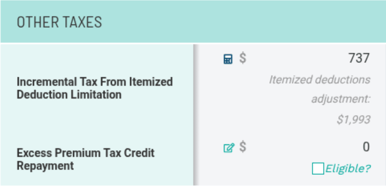

In the example below, the taxpayer has $36,485 of itemized deductions in 2026, but his income lands him in the 37% marginal bracket.

When this occurs, users will see a new line at the top of the Other Taxes section:

Clicking the calculator icon will bring up the audit for how Holistiplan arrived at the adjustment and corresponding tax:

When the IRS clarifies where taxpayers are supposed to calculate and report any limitations on itemized deductions, we will revisit our approach to confirm accuracy.

Extension of higher individual AMT exemption levels established by the TCJA

Starting in 2026, the individual Alternative Minimum Tax (AMT) rules will undergo permanent changes that extend key provisions from the Tax Cuts and Jobs Act (TCJA). The AMT exemption amounts - the portion of income shielded from the AMT calculation - will be permanently retained at the higher levels introduced under the TCJA and will continue to be adjusted annually for inflation.

However, the income thresholds at which the exemption begins to phase out will return to their lower, pre-2018 levels: $500,000 for Single filers ($1 million for Joint Filers), also indexed for inflation going forward. (Technically, these amounts are indicated as being attributed to a “base year” of 2025, which would then be adjusted for inflation in 2026 when these elements of the OBBBA are scheduled to go into effect.) Additionally, the rate at which the exemption phases out will double, from 25% to 50%.

Adjustments to Section 199A (Qualified Business Income Deduction)

The OBBBA maintained the 20% deduction of qualified business income but made two adjustments, both of which go into effect in 2026.

- First, taxpayers with at least $1,000 of Qualified Business Income (QBI) will receive a minimum QBI Deduction of $400. This minimum QBI deduction will adjust for inflation in future years.

- Second, the legislation increases the taxable income limitation phase-in amounts from $75,000 to $150,000 for Joint Filers, and from $50,000 to $100,000 for all other filing statuses. These expanded limits will apply to specified service trades or businesses (SSTBs) as well as pass-through entities subject to wage and investment limitations.

Users have no immediate action to take related to these adjustments

New Deductions

The OBBBA introduces some new deductions (additional senior deductions, car loan interest, tips, and overtime), as well as reviving charitable deductions for taxpayers who do not itemize.

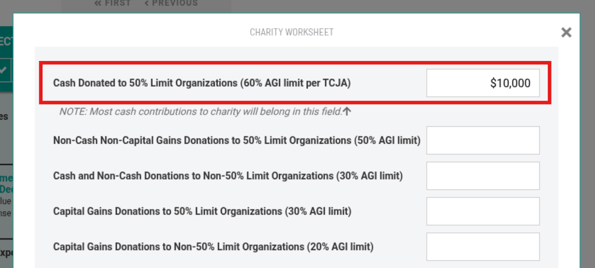

Charitable Deductions for Taxpayers Not Itemizing

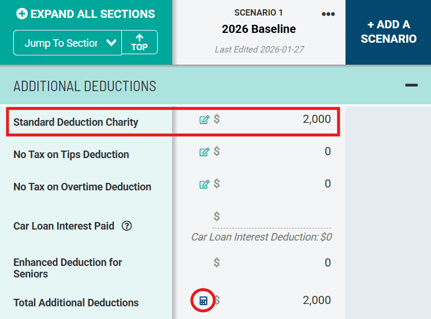

$1K (single) / $2K (MFJ). This deduction starts in 2026 and is made permanent, meaning that it is not scheduled to sunset in future years. To illustrate this deduction, enter charitable contributions in the Charity Worksheet in the Schedule A - Itemized Deductions section, specifically in the row labeled Cash Donated to 50% Limit Organizations (60% AGI Limit per TCJA). This is critical because this deduction is only available for cash contributions to charity:

The appropriate deduction amount will be displayed in the Additional Deductions section. Holistiplan will account for whether it is optimal to take those charitable deductions by itemizing on Schedule A or via the new charitable deduction for those taking the standard deduction.

Users can also click on the calculator icon circled above to see the calculation audit for any limitations on any of the new deductions reported on the new Schedule 1-A.

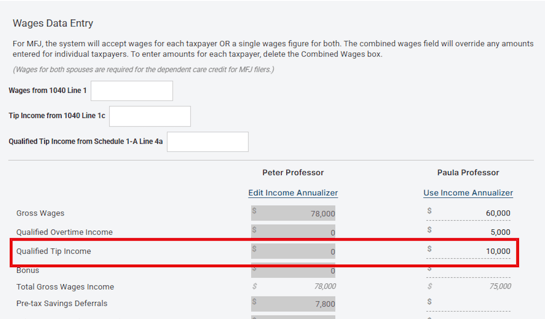

No Tax on Tips

Up to $25,000 deduction (2025-2028). For tax years 2025 through 2028, taxpayers are eligible to deduct up to $25,000 of qualified tip income. “Qualified tips” are considered cash tips received by an individual with an occupation that customarily and regularly receives tips on or before December 31, 2024. Taxpayers start to phase out of the deduction by $100 for each $1,000 by which the taxpayer’s MAGI exceeds $150,000 ($300,000 for Joint Filers). Married individuals who file a separate return are not eligible for this deduction.

Users will need to break out tip income from gross wages in the Wages worksheet and enter that tip income in the appropriate row, separated by taxpayer.

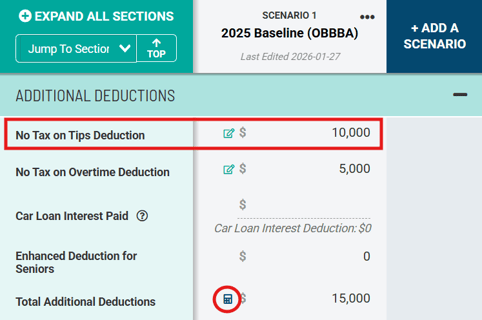

The allowable deduction amount will be calculated automatically and will show in the No Tax on Tips Deduction line item within the Additional Deductions section.

Click on the calculator icon circled above to see the calculation audit for any limitations on any of the new deductions reported on the new Schedule 1-A.

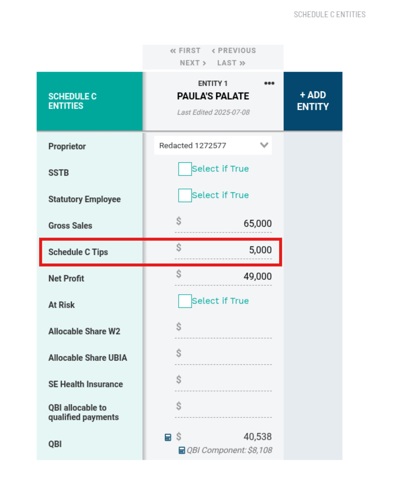

Additionally, taxpayers filing Schedule C may also be eligible for the tips deduction, assuming their business meets the same qualifying criteria. To enable the deduction, users will need to enter qualified tips received by the Schedule C filer in the appropriate row of the Schedule C Entities worksheet:

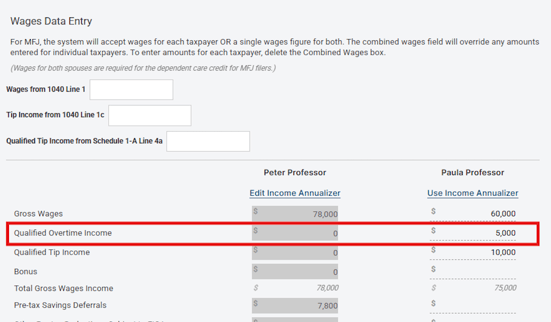

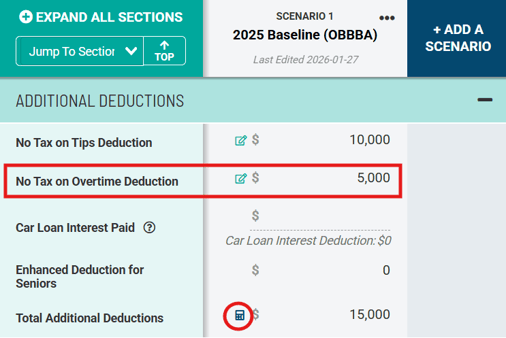

No Tax on Overtime

Up to $12,500 (Single) / $25,000 (Joint) (2025-2028). Eligible taxpayers can deduct up to $12,500 of overtime income ($25,000 for Joint Filers). Taxpayers will begin to phase out of this deduction by $100 for each $1,000 by which the taxpayer’s MAGI exceeds $150,000 ($300,000 for Joint Filers). “Qualified overtime compensation” is considered overtime compensation paid to an individual as required under section 7 of the Fair Labor Standards Act of 1938, that is in excess of the regular rate at which such individual is employed. Married individuals who file a separate return are not eligible for this deduction.

Separate any overtime income from Gross Wages in the Wages Worksheet and enter that overtime income in the appropriate row:

The allowable deduction amount will be calculated automatically and will show in Additional Deductions. Click on the calculator icon to see the calculation audit for any limitations on any of the new deductions reported on the new Schedule 1-A.

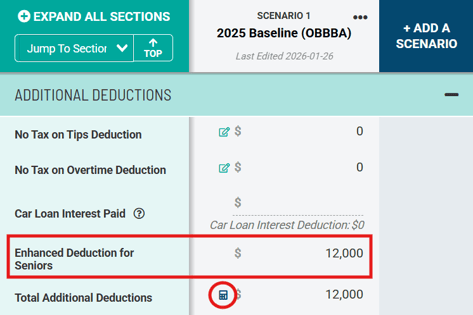

Enhanced Senior Deduction

For tax years 2025 - 2028, taxpayers age 65 and older may be eligible to take an additional deduction of up to $6,000 per person. This deduction begins to phase out at MAGI of $75,000 ($150,000 for Joint Filers) and phases out completely at MAGI of $175,000 ($250,000 for Joint Filers). Married individuals who file a separate return are not eligible for this deduction.

Holistiplan will automatically calculate the Enhanced Senior Deduction (including income-related phaseouts) and display it in the Additional Deductions section. Click on the calculator icon to see the calculation audit for any limitations on any of the new deductions reported on the new Schedule 1-A.

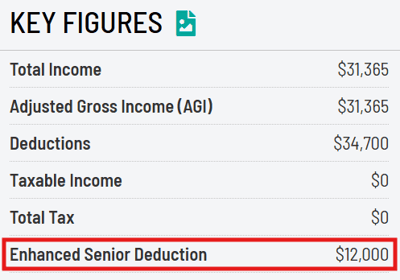

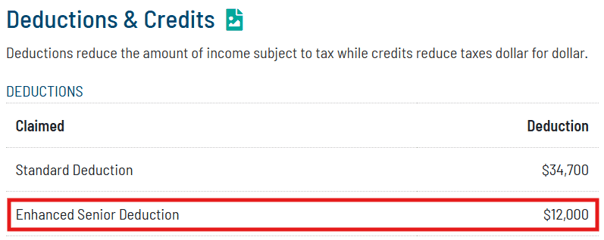

The Enhanced Senior Deduction will show in Key Figures and in the Deductions and Credits section of the Tax Report:

Caution: The Social Security Administration published a blog post on July 3, 2025, related to the passage of the OBBBA, noting, “The bill ensures that nearly 90% of Social Security beneficiaries will no longer pay federal income taxes on their benefits.” This post has created some confusion that changes were made directly related to the taxation of Social Security benefits; however, no changes were made to the way Social Security benefits are taxed.

This reference to 90% of seniors no longer paying federal income taxes on Social Security benefits appears to be related to the increase in the standard deduction. Statistically, about 90% of taxpayers utilize the standard deduction, so indirectly, the increase in standard deduction amounts and enhanced senior deductions may result in lower taxes, but not due to any direct changes to the way the taxable portion of Social Security benefits is calculated.

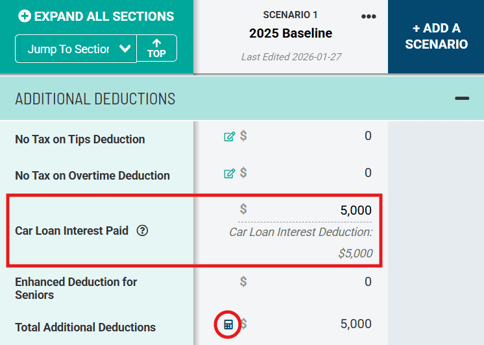

Auto Loan Interest Deduction

Starting in 2025, taxpayers will be able to deduct up to $10,000 of interest on new car purchases of cars assembled in the United States.

Taxpayers may see a limit on these deductions, as they begin to phase out by 20% when MAGI exceeds a particular income amount based on filing status:

- MFJ: Starts at $200k

- Others: Starts at $100k

To generate this deduction, enter the amount of interest paid in the appropriate row in the Additional Deductions section, and Holistiplan will calculate the appropriate deduction. Click the calculator icon circled to see how the math plays out for any additional deductions on the new Schedule 1-A.

New or Enhanced Credits

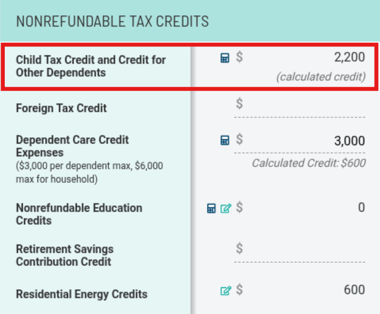

Child Tax Credit

The OBBBA increases the Child Tax Credit to $2,200 per eligible child in 2025, up from the $2,000 amount under the Tax Cuts and Jobs Act (TCJA). The credit phases out over the same MAGI range as it did in the TCJA. Holistplan automatically calculates this credit based on the user-entered number of eligible children in the Filing Status/Age/Dependents section:

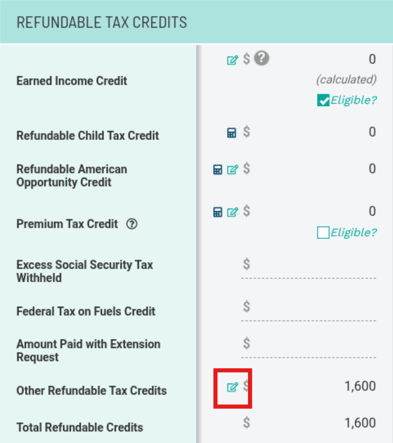

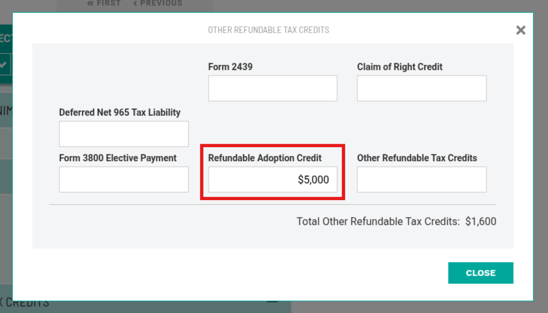

Adoption Credit

The OBBBA makes up to $5,000 of the adoption credit refundable starting in 2025 and adjusts the credit for inflation in future years. Users can find the Refundable Adoption Credit in the Other Credits modal in the Refundable Credits section.

Holistiplan will automatically calculate any income-related phaseouts of this credit. Additionally, Holistiplan will display a warning notification if users attempt to enter an amount greater than $5,000 in the Refundable Adoption Credit field.

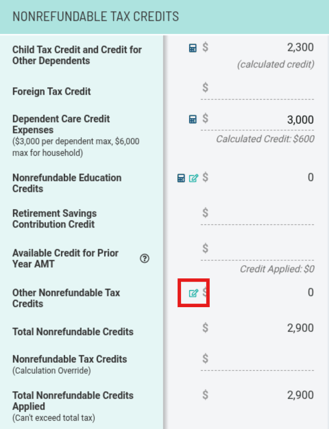

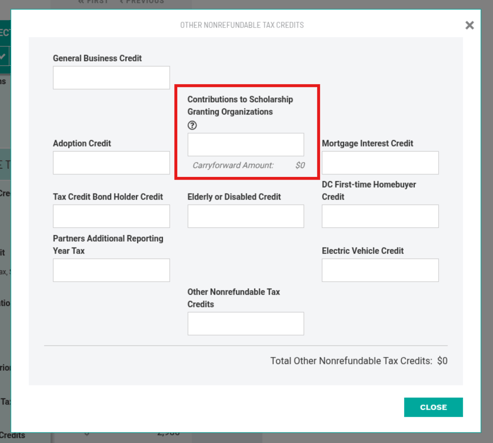

Scholarship Credit

Beginning in 2027, taxpayers can claim a non-refundable credit of up to $1,700 per year for cash donations to approved Scholarship Granting Organizations (SGOs). The credit is available to all taxpayers, including non-itemizers, and can be carried forward for up to five years if unused; however, it is reduced by any state tax credit received for the same donation, and donations claimed for this credit cannot also be deducted as charitable contributions.

Users can find the appropriate field for this credit in the Other Non-Refundable Credits worksheet in the Nonrefundable Tax Credits section:

Wrap-Up

In addition to modeling these changes in Scenario Analysis, users can also see how additional income affects the eligibility of the new deductions and credits under the new legislation. The addition of new deductions/credits and phaseouts of those means new colors and shapes within Range Calc. Read more about our Range Calc Tool in the article below.

What is Range Calc?