Despite the different rules about when RMDs begin, clients can still utilize QCDs for charitable gifting after age 70.5. The QCD Explainer is a feature available to Premium Holistiplan subscribers that helps to evaluate if using QCDs might be appropriate for your client.

Where is the QCD Explainer?

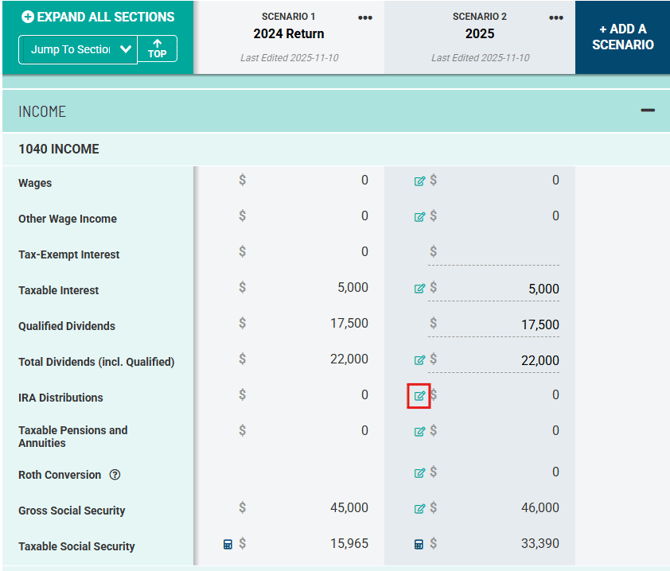

From the main Scenario Analysis screen, navigate to the "IRA Distributions" line in the "1040 Income" section. Then you will click the pencil icon circled below to access the IRA Distributions Worksheet.

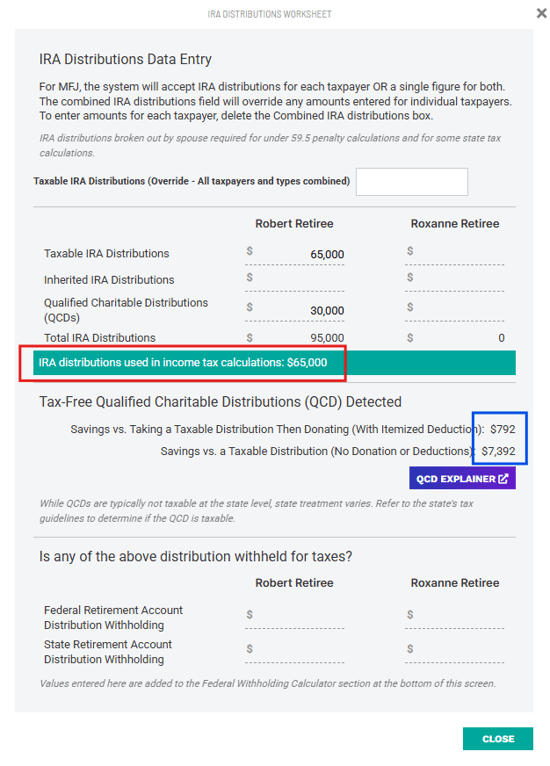

Within the IRA Distributions Worksheet, you will see options to enter taxable IRA distributions and QCDs. For example, to model $95,000 of total IRA distributions, with $30,000 being treated as a QCD, and $65,000 being treated as taxable income, you would enter those two amounts as shown below.

The IRA distribution amount that will be included in taxable income is shown outlined in red, and the tax savings are shown within the worksheet outlined in blue. Once a number is entered in the QCD portion of the IRA Distributions Worksheet, the purple QCD Explainer button will appear for you to be able to click and access the QCD Explainer.

The QCD Explainer

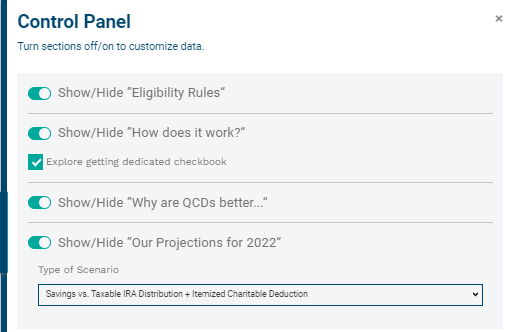

The QCD Explainer will open in the same tab. The page will feature your firm logo with a brief description of what a qualified charitable distribution is at the top of the page; four sections detailing the eligibility rules, how it works, why QCDs may be better than other alternatives, and how a QCD plays into the projections for the current tax year; followed finally with your disclaimer at the bottom of the page.

You can read about the steps to customize your logo and disclaimer in our article here.

Any of the four sections outlined below can be hidden or modified using the "Control Panel" slide out drawer found on the right side of your QCD Explainer page shown below.

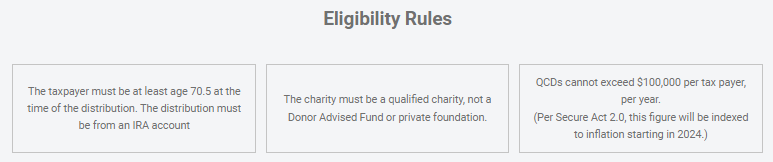

Eligibility Rules

Note: If a client turns 70.5 in the tax year you are modeling the QCD for within Scenario Analysis, you will see an additional box for those taxpayers indicating the exact date they turn 70.5 based on the date of birth entered in the client household, since QCDs are not permitted until that specific date when a client actually turns 70.5.

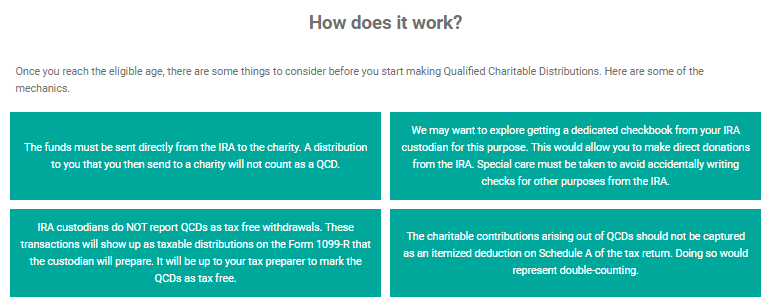

How does it work?

Why is it better?

Impact on current year projections

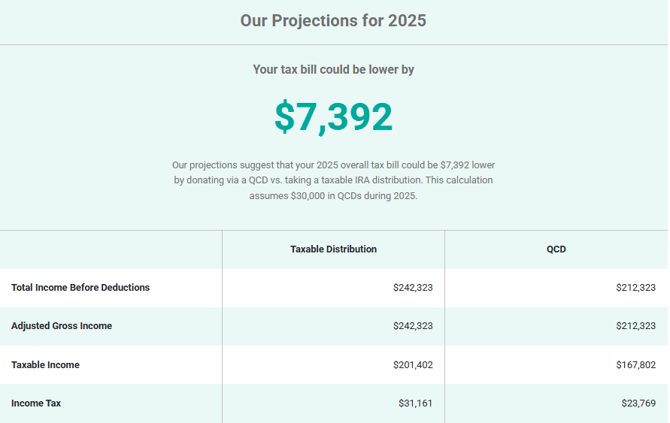

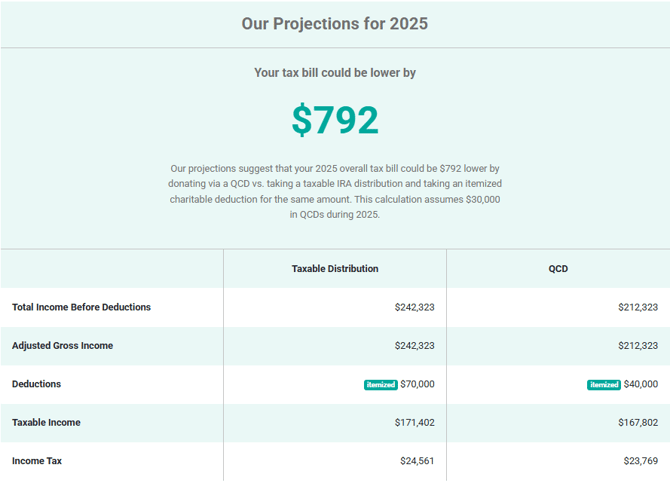

The impact on the current tax year's projections can be seen in two different ways - the savings of doing a QCD vs. making a taxable distribution, or the savings of doing a QCD vs. making a taxable distribution, and then satisfying that client's charitable intent by making a charitable contribution for the itemized deduction on Schedule A.

Savings vs. Taxable IRA Distribution Scenario

Savings vs. Taxable Distribution Scenario + Itemized Charitable Deduction

We hope you find this QCD Explainer to be a helpful tool in your advisor toolkit to navigate and explain the possible benefits to your client of utilizing Qualified Charitable Distributions as a charitable giving strategy. If you have any questions along the way, feel free to click the "Contact Support" dropdown and then "Contact Support" on the top-right of your QCD Explainer screen for assistance!