If you are working with self-employed clients, you are likely aware of the important decision they face of which business structure works best for tax purposes.

NOTE: Holistiplan does not currently support business return uploads. For S-Corps, only the net income reported on the Schedule E that is carried over to the taxpayer's Form 1040 will be used within the software.

To compare the tax implications of various entity selections, you will first want to model the business activities as a Schedule C, Partnership, or S-Corp in one scenario, and then compare that scenario with an alternative business structure. In this article, we cover:

- How to Model a Schedule C,

- How to Model an S-Corp

- How to Model a Partnership, and

- How to Compare those Entity Selections for your client

Modeling LLCs (Filing as a Schedule C):

Sole Proprietorships, Qualified Joint Ventures, and Single-Member LLCs (also referred to as disregarded entities by the IRS), as well as contract "gig" workers that receive 1099s instead of W-2 wage income generally record business activities on Schedule C. To model an LLC business type entity for your client on Schedule C, you will want to navigate to the "Schedule C Entities" Worksheet by clicking on the pencil icon shown below.

Schedule C Entities Worksheet:

Once in the Schedule C Entities Worksheet, you will see all the Schedule C Entities for that scenario. In the example below, from Peter and Paula Professor's 2023 tax return, you can click on the entity title outlined in blue to name the business entity.

You will also want to click on the "Proprietor" drop-down box also outlined in blue below, and assign the business to the appropriate taxpayer. You can assign any client that has been added to the client household as the business owner.

To add additional entities, you can click on the "+ Add Entity" button outlined in green below. This button behaves in the same way as the "+ Add A Scenario" button, in that you can create a blank entity and enter the information from scratch, or copy an existing entity.

Next, enter the information for that specific business:

- SSTB: Make a note if the business entity is a Specified Service Trade or Business (SSTB) by checking this box, if appropriate. Understanding if the business is considered an SSTB is important for the calculation of the QBI Deduction (discussed later).

- Statutory Employee: Check this box if the income from this business is paid out in the form of a W-2 (not common). Social security and Medicare tax are withheld from W-2 earnings, so you do not owe Self-Employment Tax (SE Tax) on these earnings. Statutory employees include full-time life insurance agents, certain agent or commission drivers and traveling salespersons, and certain homeworkers. If you had both SE income and statutory employee income, you would want to record any SE income here and the statutory employee income in the Wages Worksheet within the "1040 Income" section.

- Gross Sales: Enter gross sales as reported on line 7 of Schedule C.

- Net Profit: Enter net profit after all expenses, not including expenses that are reported on Schedule 1 as business-related deductions (Deductible part of SE Tax; SEP, SIMPLE, and other qualified retirement plan contributions, and SE health insurance deduction). This amount is the amount of Schedule C income subject to SE Tax.

- At Risk: Check this box if a loss is reported for this business and that loss is equal to the amount you could actually lose in the business under the at-risk rules.

- Allocable Share W-2: Indicate any statutory employee income here (see above) so that that component of business income can be accounted for with respect to the QBI Deduction on line 4 of Form 8995-A.

- Allocable Share UBIA: Indicate any allocable share of the unadjusted basis immediately after acquisition (UBIA) of all qualified property owned by the business so that that can be accounted for with respect to the QBI Deduction on line 7 of Form 8995-A.

- SE Health Insurance: If the business is providing the health insurance coverage for the owner, enter the cost of that coverage here. Holistiplan will automatically incorporate this number into Schedule 1 Deductions, and additionally, reduce QBI by this deduction as a component of the QBI Deduction calculation as well.

Schedule 1 Deductions:

From the entries in the Schedule C Entities Worksheet above, Holistiplan has now incorporated the business-related Schedule 1 Deductions outlined in blue below. In the previous iterations of Scenario Analysis, Holistiplan would calculate the QBI deduction based on your entry for QBI. With these most recent changes, Holistiplan will now calculate QBI for your Schedule C businesses based on the entries for net profit, the calculated SE Tax (and deductible portion), Self-Employed Health Insurance, and Self-Employed Plans.

In addition, to ensure that Schedule C active income is not subjected to Net Investment Income Tax (NIIT) on Form 8960, Holistiplan has also included an amount equal to the negative figure for net profit in the "Other Taxes" section as well. *NOTE: Beginning with Tax Year 2022, the Instructions for Form 8960 include Schedule C income as listed on line 3 of Schedule 1 on line 4a and require it to be backed out on line 4b.

The only remaining entry needed for Schedule C will be to incorporate any contributions to SE-qualified retirement plans (such as SEP, Solo 401(k) contributions, or SIMPLE IRA plans). As part of our Schedule C modeling upgrade in April 2024, we have incorporated a new "Self-Employed Plans" Worksheet.

Within the new worksheet, you can enter the self-employed plan contributions where shown outlined in green below. You'll notice that we have also incorporated a popular request as well, as we'll note the maximum SEP Contribution, Solo 401(k) Contribution, or SIMPLE IRA Contribution that your self-employed client can make from their SE income. The entry here will roll back into the "Schedule 1 Deductions" section, and your client's QBI Deduction for Schedule C will recalculate automatically. No more manual adjustments to get to the correct QBI!

NOTE: While we will call out the maximum SEP, Solo 401(k), or SIMPLE IRA contributions your client can make from SE Income, if you enter a SE plan contribution and later make changes to business income, please revisit this SE Plan Contributions section to ensure your entry is still within the max contribution limits.

Also, if your client has multiple 401(k)s or SEP accounts, be sure to be mindful of the overall aggregate plan limits across plan types as stated by IRS §415(c).

Qualified Business Income (QBI) Deduction Calculation:

At this point, you have accounted for the income and expenses for Schedule C, net profit, SE Tax, the deductible portion of SE Tax, and any SE Health Insurance deduction or deduction for contributions from SE income to qualified retirement plans. Holistiplan has incorporated those entries into our calculation for QBI and the QBI deduction.

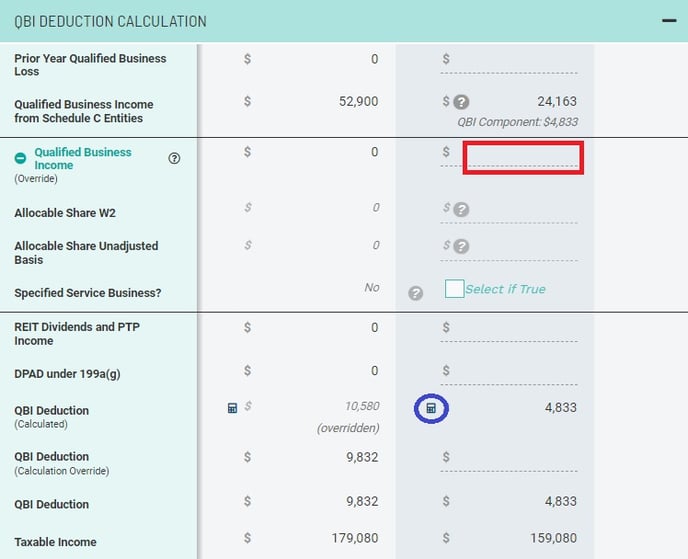

In the example below, the new QBI for Paula's Schedule C business is $24,163. The calculated deduction of $4,833 can be seen just below the QBI. If you wanted to double-check the math behind the scenes of that QBI deduction, you can click on the calculator icon circled below for an audit of that calculation as it flows through Form 8995 or Form 8995-A.

The QBI (Override) field outlined in red needs to be used only if your client has QBI from both Schedule C and Schedule E sources. If your client only has QBI from Schedule C, you can leave this field blank.

If your client has QBI from Schedule C and Schedule E, you will want to combine the QBI from the Schedule C Entities with any Schedule E QBI in the "Self Employed Key Figures" Worksheet with the QBI as calculated for your client's Schedule C entities, and enter that combined figure into the field outlined in red above.

Modeling S-Corps:

An S-Corp is not an entity, but an election that passes corporate income, losses, deductions, and credits through to shareholders for federal tax purposes. This necessitates a separate corporate return to report business income - Form 1120-S. The S-Corp return then issues K-1s to all shareholders to reflect their portion of business income on the individual shareholders' tax returns. To model S-Corp business activities, you will use the Self-Employment Key Fields Worksheet, but there are a few additional wrinkles.

- Wages Worksheet:

An S-Corp owner needs to pay himself/herself reasonable compensation in the form of an appropriate amount of wages, which would be entered at the top of the "1040 Income" section in the Wages Worksheet, where shown below:

- Self-Employment Key Fields Worksheet:

The remaining business income is distributed as net income to the S-Corp shareholders via a K-1, which is generally entered as Schedule E income. However, a K-1 can distribute interest/dividend income or capital gains as well, which would be entered as interest/capital gains in the '1040 Income' section or as capital gains in the 'Schedule D Income' section. This net income is not subject to SE Tax; however, unlike a Schedule C in the above LLC example, net income for the S-Corp will have to factor in all of the business' expenses, including wages paid to employees (including the shareholders/owners), employer retirement/health plan contributions, the employer's share of FICA on the reasonable compensation paid as wages, etc. You will enter that net income where outlined in blue below.

To ensure that any active business income is not subjected to Net Investment Income Tax, you will want to include the negative net profit in the "Adjustments for Net Investment Income" field outlined in yellow.

Since S-Corp income is not subject to Self-Employment (SE) Tax, provided there are no other sources of SE income, the SE tax as outlined in green above should be $0.

- Holistiplan does not currently support calculating Net Income for S-Corps. Only the net income is entered in the Self-Employment Key Fields Worksheet, and no income or expense details are considered. You may choose to use our calculation rows within our Field Notes feature to note those details.

- Employer contributions to a retirement plan will be reflected on the partnership's tax return and not the personal tax return. Employee salary deferrals to retirement plans are reflected in the Wages Worksheet.

Modeling Partnerships:

Partnerships are modeled the same way as S-Corps, with one main difference - Self-Employment (SE) Taxes. Partnerships file a separate Form 1065 return, but unlike S-Corps, partnership income is subject to SE Tax in the same way that Schedule C income is. The partnership files a separate corporate return to report business income - Form 1065. The partnership return then issues K-1s to all shareholders to reflect their portion of business income on the individual shareholders' tax returns. To model partnership business activities, you will use the Self-Employment Key Fields Worksheet.

- Self-Employment Key Fields Worksheet: The net business income is distributed to partners via a K-1, which is generally entered as Schedule E income. However, a K-1 can distribute interest/dividend income or capital gains as well, which would be entered as interest/dividend income in the '1040 Income' section or as capital gains in the 'Schedule D Income' section. This net income is subject to SE Tax, and the partnership's net income will have to factor in all of the business's expenses, including wages paid to employees (including the shareholders/owners), employer retirement/health plan contributions, the employer's share of FICA, etc. You will enter that net income where outlined in blue below.

To ensure that any active business income is not subjected to Net Investment Income Tax, you will want to include the negative net profit in the "Adjustments for Net Investment Income" field outlined in yellow.

To reflect the partnership's exposure to SE Tax, you would include any partnership net income in the "Other Self-Employment Income" field above in the Self-Employment Tax section of the Self-Employment Key Fields Worksheet.

- Holistiplan does not currently support calculating Net Income for partnerships. Only the net income is entered in the Self-Employment Key Fields Worksheet, and no income or expense details are considered. You may choose to use our calculation rows within our Field Notes feature to note those details.

- Employer contributions to a retirement plan will be reflected on the partnership's tax return and not the personal tax return.

Qualified Business Income (QBI) Deduction Calculation:

If there are QBI Sources outside of Schedule C Entities, Holistiplan cannot currently calculate any part of QBI automatically. Instead, we suggest using an external calculator to determine the total QBI, which you can enter in the field outlined in blue below. Holistiplan will then calculate the QBI deduction based on that manually entered QBI.

Generally, QBI will be equal to net income from that Schedule E activity, but you can use the fields in the drop-down of this row if any of the following items apply in your scenario.

- Allocable Share W-2: Indicate any statutory employee income here (see above) so that that component of business income can be accounted for with respect to the QBI Deduction on line 4 of Form 8995-A.

- Allocable Share UBIA: Indicate any allocable share of the unadjusted basis immediately after acquisition (UBIA) of all qualified property owned by the business so that that can be accounted for with respect to the QBI Deduction on line 7 of Form 8995-A.

- SSTB: Make a note if the business entity is a Specified Service Trade or Business (SSTB) by checking this box, if appropriate. Understanding if the business is considered an SSTB is important for the calculation of the QBI Deduction.

Compare Tax Implications of Various Business Forms:

Once you have modeled out two or more scenarios for your client's business income, you can utilize our Comparison Tool to compare the tax implications of one business incorporation option vs. another.

Keep in mind that the employee-side cost of payroll taxes is a consideration when evaluating the decision to elect an S-Corp status. Holistiplan can reflect these additional costs on the 'Tax Plus FICA' line in Scenario Analysis as described in our FICA in Holistiplan article, if the Wages Worksheet has been entered appropriately.

Other non-tax considerations when determining which business entity form is appropriate for your client that cannot be modeled in Holistiplan involve added administrative and tax preparation costs. Although those cannot be modeled, those considerations may factor into your decision as well.

If you have any questions along the way as you model these scenarios out within Holistiplan, please Contact our Support Team for further assistance!